NABTEB 2026 Financial Accounting Questions & Answers (Paper 423)

This page contains the NABTEB 2026 Financial Accounting questions and answers for Paper 423, covering Section A (Objective, 25 marks, 1 hour) and Section B (Essay questions). You will find the official question paper images first, followed by the complete answer key and worked solutions where possible.

NABTEB 2026 Financial Accounting — Official Question Paper (Images)

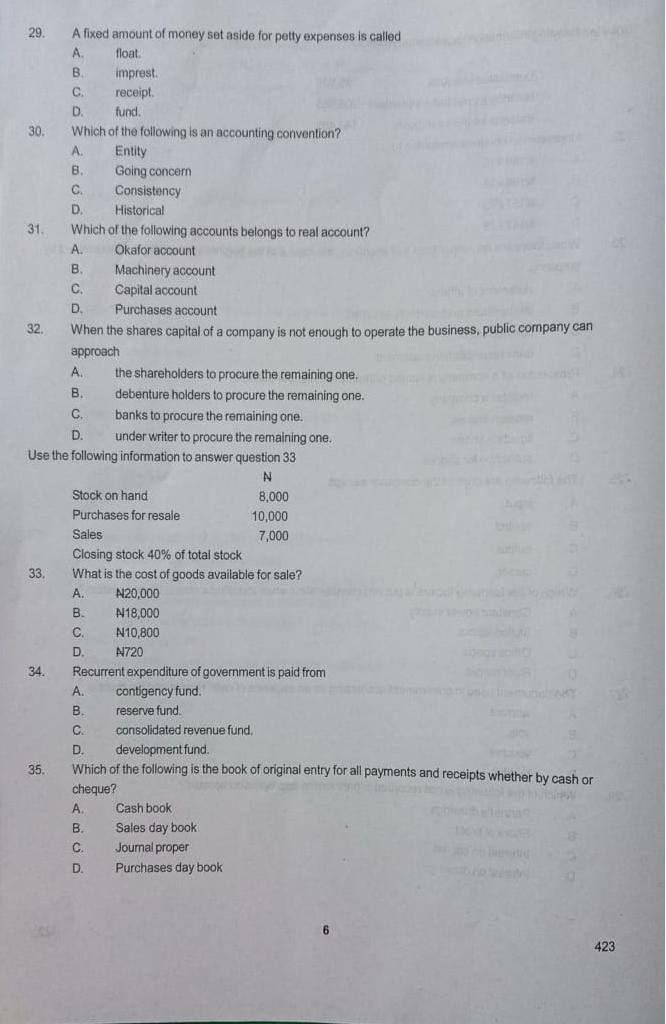

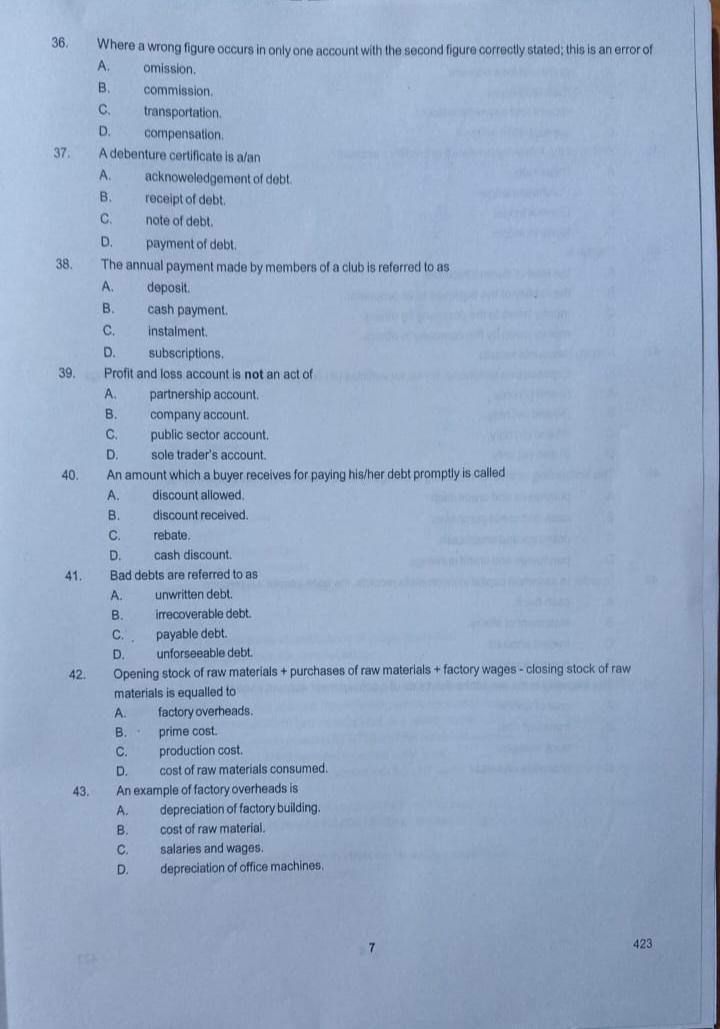

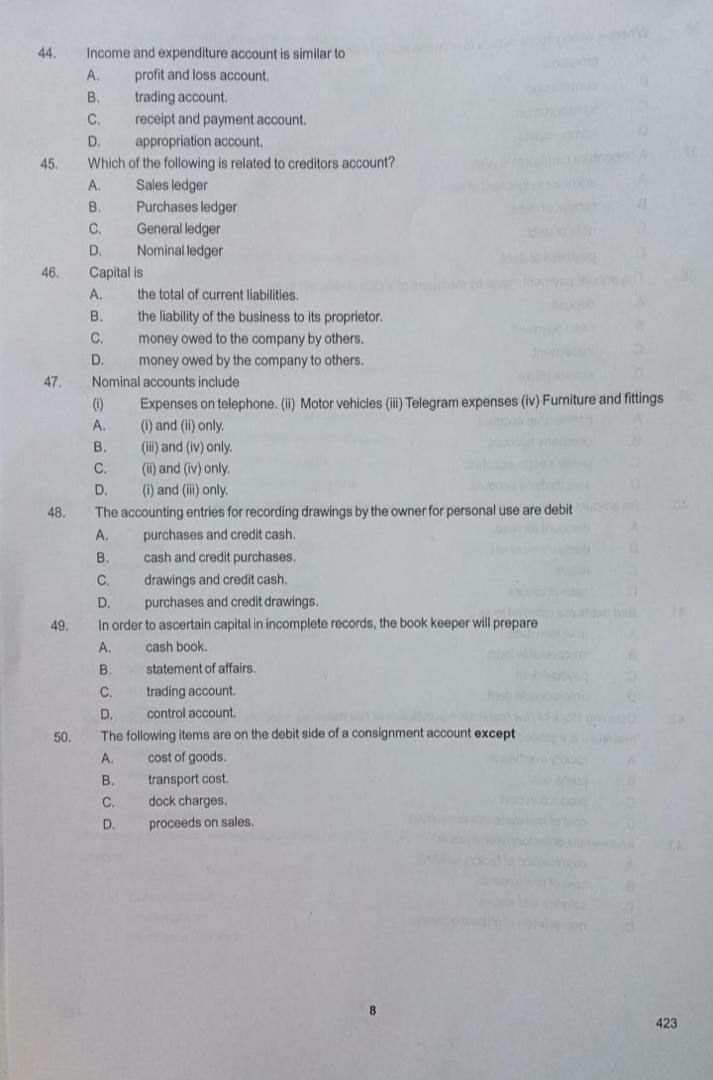

SECTION A — Objective Answers (50 Questions)

Below are the suggested correct options for all 50 multiple-choice questions from Section A of the 2026 NABTEB Financial Accounting Paper 423, based on the official question paper shown above.

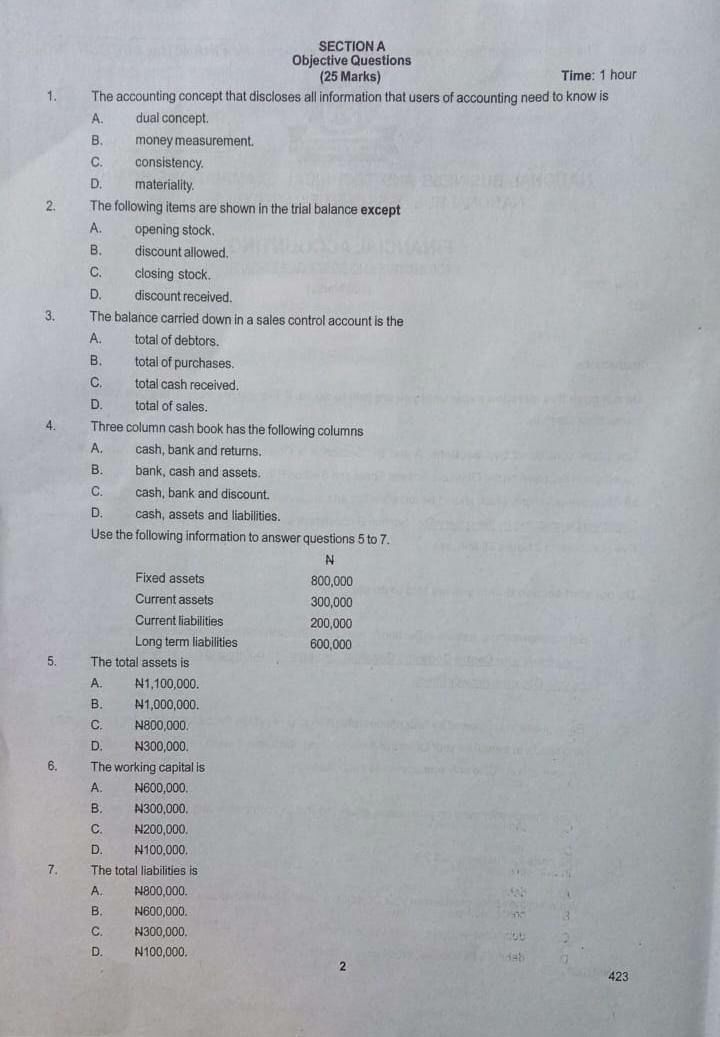

- Q1 → D

- Q2 → C

- Q3 → A

- Q4 → C

- Q5 → A

- Q6 → D

- Q7 → B

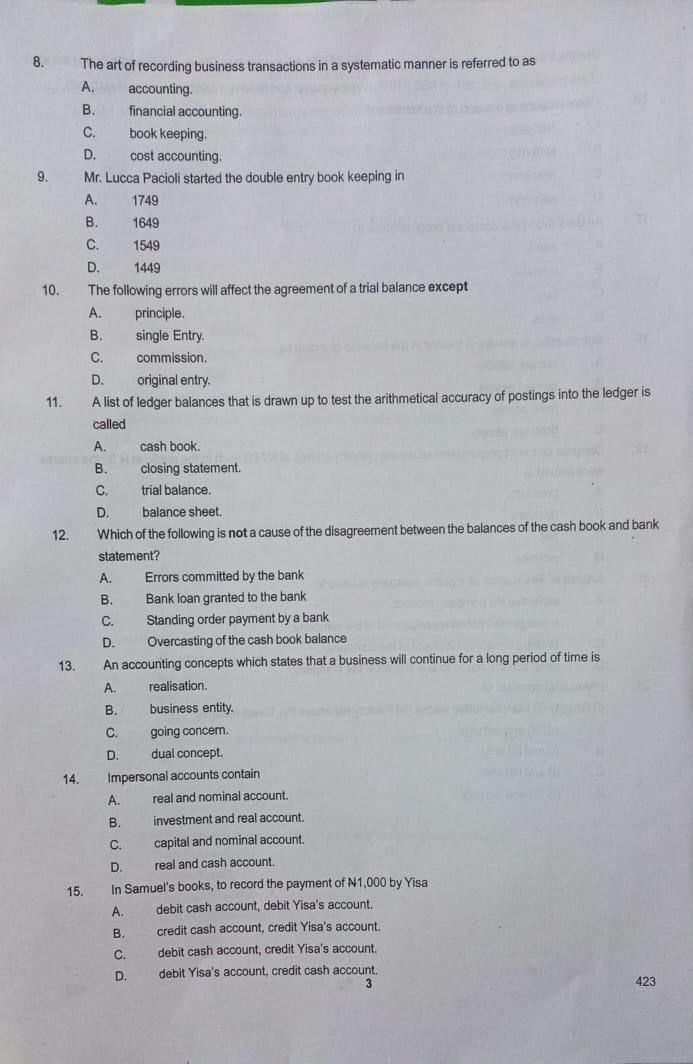

- Q8 → A

- Q9 → B

- Q10 → B

- Q11 → C

- Q12 → B

- Q13 → C

- Q14 → A

- Q15 → C

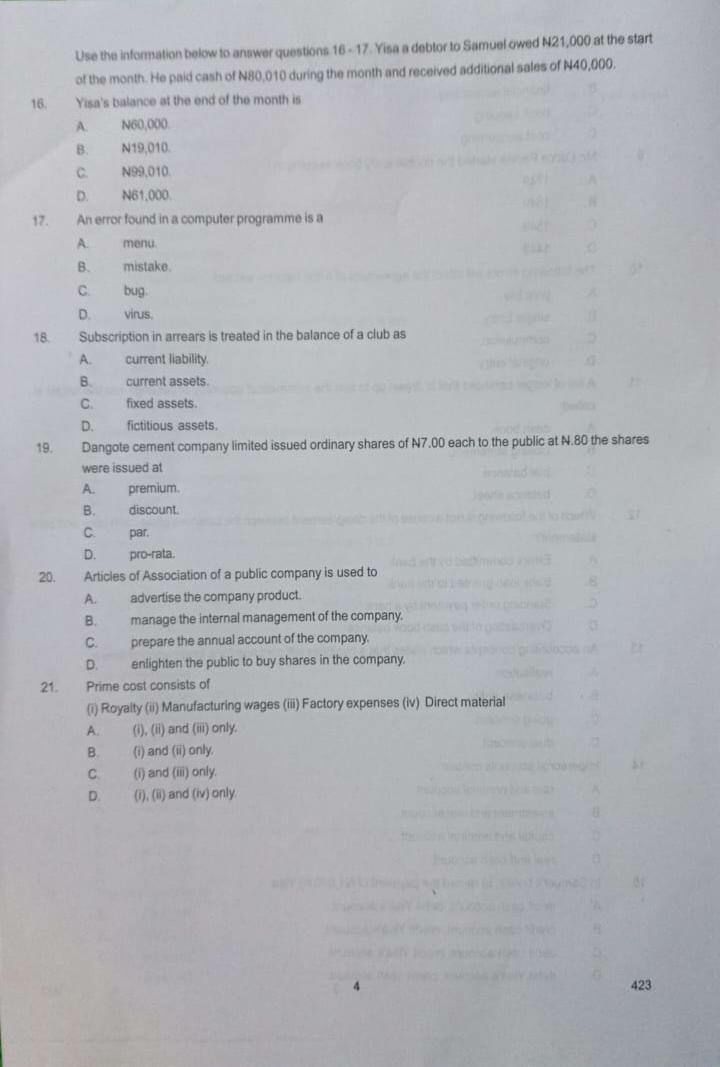

- Q16 → B

- Q17 → C

- Q18 → A

- Q19 → A

- Q20 → B

- Q21 → D

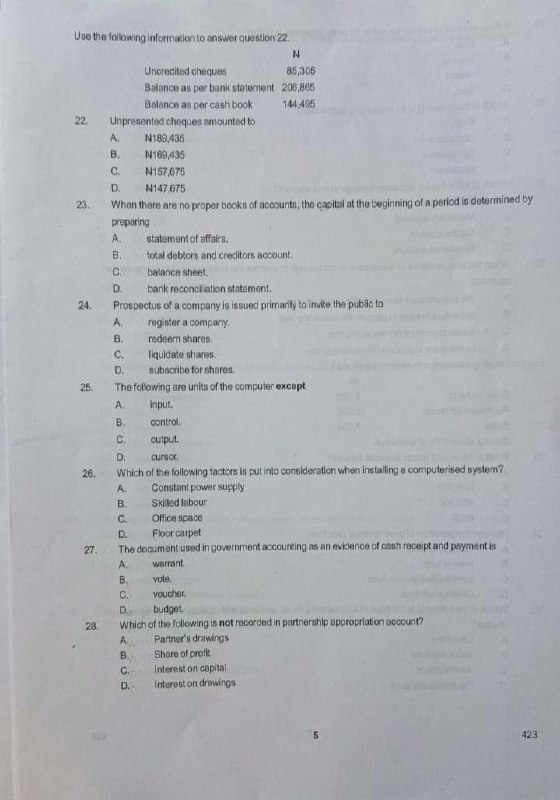

- Q22 → C

- Q23 → A

- Q24 → D

- Q25 → D

- Q26 → A

- Q27 → C

- Q28 → A

- Q29 → B

- Q30 → C

- Q31 → C

- Q32 → D

- Q33 → B

- Q34 → C

- Q35 → A

- Q36 → B

- Q37 → A

- Q38 → D

- Q39 → D

- Q40 → B

- Q41 → B

- Q42 → B

- Q43 → A

- Q44 → A

- Q45 → B

- Q46 → B

- Q47 → D

- Q48 → C

- Q49 → B

- Q50 → D

SECTION B — Essay Questions and Worked Solutions

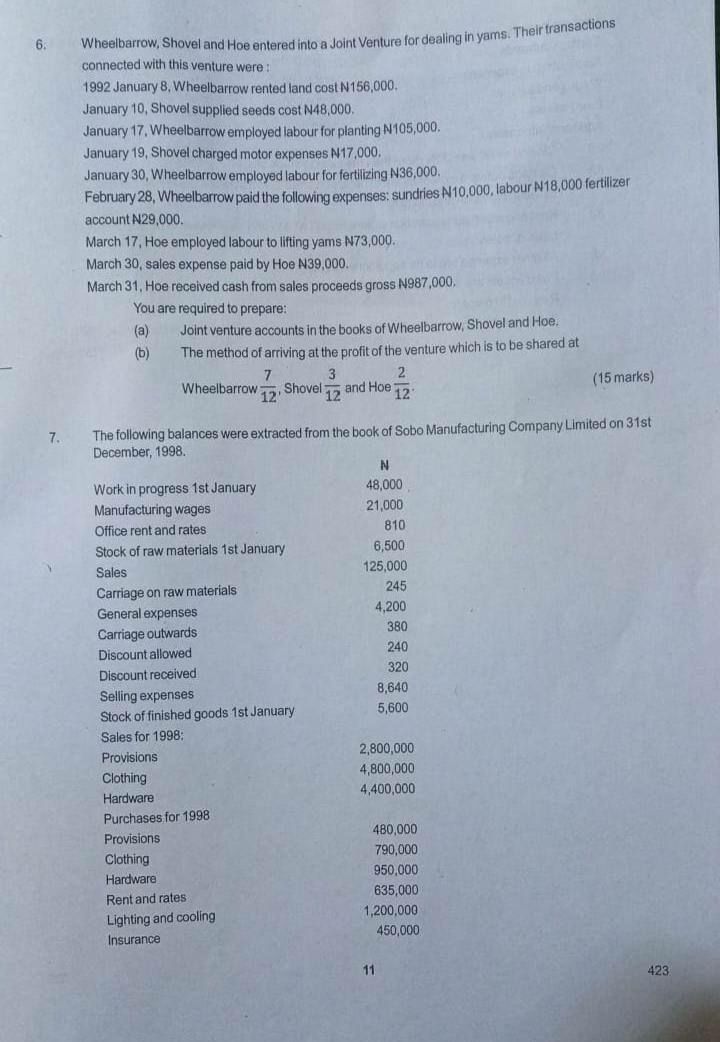

Question 6 — Joint Venture (15 Marks)

Requirement: Prepare the Joint Venture accounts in the books of Wheelbarrow, Shovel and Hoe and show the method of arriving at the profit to be shared.

Given data (summary):

- Wheelbarrow: Land rent — ₦156,000; Labour (planting) — ₦105,000; Labour (fertilizing) — ₦36,000; Sundries — ₦10,000; Labour (Feb 28) — ₦18,000; Fertilizer — ₦29,000.

- Shovel: Seeds — ₦48,000; Motor expenses — ₦17,000.

- Hoe: Labour lifting yams — ₦73,000; Selling expenses — ₦39,000; Cash from sales (gross proceeds) — ₦987,000.

- Profit sharing ratio: Wheelbarrow 7/12, Shovel 3/12, Hoe 2/12.

1. Total Joint Venture Expenses

- Wheelbarrow: 156,000 + 105,000 + 36,000 + 10,000 + 18,000 + 29,000 = ₦354,000.

- Shovel: 48,000 + 17,000 = ₦65,000.

- Hoe: 73,000 + 39,000 = ₦112,000.

- Total expenses = 354,000 + 65,000 + 112,000 = ₦531,000.

2. Memorandum Joint Venture Account (for profit computation)

Memorandum Joint Venture Account

Dr Cr

Joint Venture (Memorandum)

Details ₦ Details ₦

-------------------------------- --------------------------------

To Wheelbarrow exp. 354,000 By Sales proceeds (Hoe) 987,000

To Shovel exp. 65,000

To Hoe exp. 112,000

Total expenses 531,000

Profit on joint

venture (bal. fig.) 456,000

------ -------

987,000 987,000

3. Sharing of Profit (₦456,000)

- Wheelbarrow: 7/12 × 456,000 = ₦266,000.

- Shovel: 3/12 × 456,000 = ₦114,000.

- Hoe: 2/12 × 456,000 = ₦76,000.

4. Joint Venture Account in the Books of Each Venturer

(a) In the books of Wheelbarrow

Dr Cr

Joint Venture with Shovel & Hoe

(in Wheelbarrow's books)

Details ₦ Details ₦

-------------------------------- --------------------------------

To Bank (land rent) 156,000 By Shovel (expenses) 65,000

To Bank (labour) 105,000 By Hoe (expenses) 112,000

To Bank (fertilizer) 36,000 By Hoe (sales proceeds) 987,000

To Bank (sundries) 10,000

To Bank (labour) 18,000

To Bank (fertilizer) 29,000

To Profit & Loss

(Wheelbarrow share) 266,000

------ -------

620,000 1,164,000

Balance due to Wheelbarrow from

Joint Venture (net cash from Hoe) 544,000

Note: In many exam presentations, the personal accounts of Shovel and Hoe are opened separately in Wheelbarrow’s books to show amounts due to or from co-venturers, but the key point is that Wheelbarrow records its own cash expenses on the debit side and its share of profit on the credit side of the Joint Venture account.

(b) In the books of Shovel

Dr Cr

Joint Venture with Wheelbarrow & Hoe

(in Shovel's books)

Details ₦ Details ₦

-------------------------------- --------------------------------

To Bank (seeds) 48,000 By Bank (profit share) 114,000

To Bank (motor exp.) 17,000

To Wheelbarrow

(for balancing) 49,000

------ -------

114,000 114,000

(c) In the books of Hoe

Dr Cr

Joint Venture with Wheelbarrow & Shovel

(in Hoe's books)

Details ₦ Details ₦

-------------------------------- --------------------------------

To Bank (labour) 73,000 By Bank (sales proceeds) 987,000

To Bank (selling exp.) 39,000

To Wheelbarrow &

Shovel (expenses) 419,000

To Profit & Loss

(Hoe share of profit) 76,000

------ -------

607,000 987,000

Balance due from Hoe

to co-venturers (cash

remitted/settlement) 380,000

5. Method of Arriving at Profit

- All expenses incurred by the venturers are debited to the memorandum Joint Venture account.

- All sales proceeds are credited to the memorandum Joint Venture account.

- The balancing figure represents the profit on the joint venture.

- This profit is then shared among the venturers in the agreed ratio: 7/12 to Wheelbarrow, 3/12 to Shovel and 2/12 to Hoe.

Question 7 — Manufacturing Account

The visible part of the question provides only a portion of the information needed to prepare a complete Manufacturing, Trading and Profit & Loss account. Below is how to structure the Manufacturing Account using the figures that are available from the question paper image.

Given (from the visible data)

- Work in progress, 1 Jan — ₦48,000

- Manufacturing wages — ₦21,000

- Office rent and rates — ₦810

- Stock of raw materials, 1 Jan — ₦6,500

- Carriage on raw materials — ₦245

- General expenses — ₦4,200

- Carriage outwards — ₦380

- Discount allowed — ₦240

- Discount received — ₦320

- Selling expenses — ₦8,640

- Stock of finished goods, 1 Jan — ₦5,600

- Sales for 1998 (by department): Provisions ₦2,800,000; Clothing ₦4,800,000; Hardware ₦4,400,000

- Purchases for 1998 (by department): Provisions ₦480,000; Clothing ₦790,000; Hardware ₦950,000

- Rent and rates — ₦635,000

- Lighting and cooling — ₦1,200,000

- Insurance — ₦450,000

Important items such as closing stocks, factory power, factory depreciation and closing work in progress are not visible on the page, so a full numerical solution cannot be completed with certainty. However, the format and the use of the available figures can still be shown.

Manufacturing Account for the year ended 31 December 1998 (Extract / Format)

Dr Cr

Sobo Manufacturing Company Ltd

Manufacturing Account

for the year ended 31 Dec 1998 (Extract)

Details ₦ Details ₦

-------------------------------- --------------------------------

To Opening stock of

raw materials 6,500 By Closing stock of

To Purchases of raw materials (b/f)

raw materials (b/f)

To Carriage on raw

materials 245

Raw materials

available for use (bal.)

Less: Closing stock

of raw materials (b/f)

------

Raw materials

consumed (bal.)

To Manufacturing wages 21,000

To Work in progress,

1 Jan 48,000

To Factory overheads:

(portion of rent &

rates, lighting &

cooling, insurance,

general expenses, etc.)

(b/f)

------ By Work in progress,

31 Dec (if given) (b/f)

Cost of production

of finished goods (bal.) By Finished goods

(to Trading A/c) (bal.)

------ -------

xxxx xxxx

Notes:

- Only the factory-related portion of rent and rates, lighting and cooling, insurance and general expenses should be charged to the Manufacturing Account. The remaining portions would go to the Trading or Profit & Loss Account, depending on the instructions in the full question.

- Carriage on raw materials is treated as part of the cost of raw materials consumed and therefore debited to the Manufacturing Account.

- Carriage outwards, selling expenses and discount allowed are selling and distribution costs and appear in the Profit & Loss Account, not in the Manufacturing Account.

- Discount received is an income item credited in the Profit & Loss Account.

- Without the closing stocks and full overhead analysis (which are on the missing part of the page), the exact cost of production cannot be computed; in an exam you would use all additional figures given on the full question paper.

Get More NABTEB & Other Exam Updates

For more NABTEB, WAEC, NECO and JAMB questions, answers and exam tips, follow ExamSmooth on WhatsApp and Telegram:

Leave a comment